The 2026 Off-Plan Playbook

How to underwrite resale risk before buying into the next launch.

It is early 2023.

A buyer walks into a sales gallery in Dubai. The lights are bright, the model is immaculate, and the broker has a story he has told a hundred times.

Buy now in phase one. Pay 10% down. The developer raises prices in phase two, then phase three.

Sell your unit before handover and walk away with a tidy gain, having never paid more than a fraction of the price.

For a while, that story was true. It worked because the next buyer always showed up.

But 2026 is a different market. The question is no longer “will this launch sell?”

Launches are still selling. The harder question, the one that actually determines whether your money is safe, is this: who buys this unit from me next?

Launch demand tells you whether a project can sell. Resale liquidity tells you whether the investment can survive.

Today I’m writing about the difference between the two.

Before we start, one thing. Further down, I’ve done something I haven’t done before.

I’ve taken the entire underwriting framework in this piece and packaged it into a Claude Skill: a one-click tool that turns Claude into a skilled analyst.

You drop in your data from Property Monitor, REIDIN, or Buildable, name a unit or project, and it scores the exit out of 100, names the buyer after you, and stress-tests the deal three ways, refusing to fake the numbers it doesn’t have.

If you want to get the tool, jump straight to the last section.

Today’s Brief:

Why launch velocity and exit liquidity have stopped being the same thing

The old off-plan playbook, and the single assumption it depended on

The new question: who is the buyer after you?

The 2026 Off-Plan Exit Framework: ten checks before you commit

Who still wins, and who is most exposed

Where AI actually earns its place in this workflow

The market is not failing. It is changing the test.

Dubai’s off-plan market is still moving serious volume.

In Q1 2026, the city recorded roughly 44,200 residential sales worth AED 139.1 billion, with off-plan accounting for 73% of all transactions. Sales value was actually up 21.5% year-on-year. By the headline numbers, this looks like a market in rude health.

But the important detail is not the headline. It is inside the off-plan number.

In Q1 2026, initial developer sales made up 91.7% of off-plan transactions, while off-plan resales fell to just 8.3%, down from 15.7% a year earlier. Nine out of ten off-plan deals are people buying directly from developers. Barely one in ten is an investor selling their off-plan unit to someone else.

By December 2025, off-plan resales had slipped to a 24.5% rolling average of all resale transactions, well below earlier peaks, which reads as longer holding periods and less flipping. The Financial Times, citing Property Monitor, reported that flipping of unfinished units had already cooled from roughly a third of the resale market to about 20% by mid-2025.

So developer merchandising is strong. The launch room still works. But the secondary exit, the part of the trade where the investor actually gets paid, is getting narrower.

Three forces are converging to make this matter now.

First, supply. 2025 was a record year for launches: over 167,000 units across 648 projects, the equivalent of a new project every 13.5 hours. That created an enormous future stack. The market is expecting 77,500 units for delivery in 2026, then roughly 146,400 in 2027 and 120,100 in 2028. And 84.3% of 2026’s projected deliveries are apartments.

Second, momentum is cooling. Rents grew 10.2% year-on-year in Q1 2026, the slowest annual pace since Q4 2022. Sales price growth, at 9.6% year-on-year, was the slowest since Q1 2023. The blanket price-and-rent support that covered sloppy underwriting in 2023 and 2024 is no longer there for every unit.

Third, the March 2026 regional shock. Reuters reported UAE transaction volumes fell 37% year-on-year in the first 12 days of March. I would treat this as a stress test, not a structural break. The conflict did not create the supply and absorption questions. It exposed how quickly confidence-sensitive secondary activity can wobble when those questions are already in the air.

The cleanest way to describe the market: it is moving from a launch-led phase to an absorption-led phase. In that market, the only question that matters is not whether you can buy. It is whether you can get out.

The old playbook, and the assumption it hid

The old off-plan trade was elegant. Here is why it worked.

You bought early, at launch pricing, often the cheapest the unit would ever be. The payment plan meant low initial cash outlay, sometimes 10% or 20% down, with the balance spread across construction. The developer then raised prices in later phases, marking up your paper value. You sold the assignment before handover, before the final cash calls, and recycled the proceeds into the next launch.

Low capital in. Visible developer-led price appreciation. An exit before the expensive part. In a rising market, with confidence high and population growth strong, mistakes got covered. Brokers could always point to momentum.

But the whole structure rested on one assumption that nobody wrote down: there will always be a next buyer who wants this unit at a higher price.

When launches were relatively scarce and rents were climbing fast, that assumption held. The next buyer was easy to imagine. Today, with a record pipeline of similar units arriving and developers still selling fresh stock with fresh payment plans, that assumption deserves scrutiny on every single deal.

The new playbook: underwrite the buyer after you

The new discipline: before you buy off-plan in 2026, define the specific buyer who takes you out.

Run through the candidates honestly:

An end-user who wants to live there

A yield investor buying for rental income

An international cash buyer

An owner-occupier family trading up

A short-term rental operator

Another speculator looking to flip again

A broker-led resale buyer

A distressed or opportunistic buyer hunting discounts

Here is the test. If the only honest answer is “another investor who wants to flip it again,” you may not have an investment thesis. You may have a game of pass-the-parcel, and the music is getting quieter.

A real exit thesis names the buyer, their cheque size, their financing route, and the reason they choose your unit over the alternatives. Everything below is a structured way to pressure-test exactly that.

The 2026 Off-Plan Exit Framework

Ten checks. Run them before you commit capital, not after. The goal is not to predict prices perfectly. It is to find where the exit is fragile before you buy the entry.

A. The supply test

What it means: Measure how much directly comparable stock is scheduled to hand over in your micro-market around your likely exit window.

Why it matters: The risk is not “too much Dubai supply” in the abstract. It is too many near-identical studios, one-beds, and generic two-beds arriving into the same corridor at the same time. Dubai’s pipeline is overwhelmingly apartment-led, which is precisely the product most vulnerable to this.

Questions to ask: How many similar units are due 12 months either side of my handover? Am I competing with five towers or fifty? Is the supply clustered in my exact budget band?

Red flags: Generic apartment corridor, hundreds of comparable units, multiple launches in the same price bracket.

Green flags: Low comparable supply, differentiated product, a community that is already largely absorbed, limited future land release.

This is exactly the kind of forward-supply mapping Buildable automates, so you're working from a real pipeline count rather than a guess.

B. The launch competition test

What it means: Underwrite not just resale competition from other investors, but the developer’s ability to keep selling brand-new alternatives with better terms.

Why it matters: A reseller asking for a cash-heavy assignment is at an instant disadvantage if the developer down the road is selling a similar unit at a similar headline price but with a friendlier post-handover payment plan. This is already visible: in the ready segment, initial developer sales rose to 18.2% of activity in Q1 2026, up from 13.7% a year earlier. Resellers are competing with developers even in finished stock.

Questions to ask: Will the developer still be selling at my exit? Are there newer launches nearby with lower entry cheques? Has the developer paused launches or are they still pushing fresh inventory?

Red flags: Same developer still selling adjacent phases, better post-handover plans on offer, reseller forced to ask for a large immediate top-up.

Green flags: Project largely sold out, no competing adjacent phases, completion near and developer stock thin.

A buyer-after-you does not compare your unit to last year’s brochure. They compare it to what the developer can sell them today.

C. The price gap test

What it means: Compare your implied exit price to actual transacted ready prices, not aspirational asking prices, for the same product in the same community.

Why it matters: If your off-plan resale needs to clear at a large premium to finished stock, the buyer asks an obvious question: why not just buy the completed unit? With apartment price momentum slowing, and ValuStrat reporting apartment values posted their first annual decline in six years in May 2026, the cushion is thinner than it was.

Questions to ask: What is the current ready price per square foot for true comparables? What premium am I assuming at resale, and is it justified by layout, brand, view, or payment plan?

Red flags: Resale assumption materially above nearby ready evidence, premium justified only by “future potential.”

Green flags: Tight gap to ready comps, premium backed by genuine scarcity or superior spec.

Force the deal to survive under a ready-market anchor.

D. The mortgage and finance test

What it means: Work out whether the buyer after you can realistically finance the purchase, and on what terms.

Why it matters: Finance defines the size of your buyer pool. The UAE Central Bank caps off-plan mortgages at 50% loan-to-value, regardless of purpose, value, or category of purchaser. That means a financed buyer near handover needs far more equity than many assume. And Savills reported mortgage transactions fell to 1,516 in March from roughly 1,900 in each of the prior two months, a narrowing of the take-out pool exactly when sentiment wobbled.

Questions to ask: Can a non-cash buyer finance this before or at handover? What completion stage do lenders require? How much actual cash must the next buyer bring?

Red flags: Unit only works for all-cash buyers, limited bank appetite, buyer needs 50%-plus equity plus fees.

Green flags: Eligible developer and project, bank appetite present, handover timing aligned with a normal mortgage transfer.

If your exit requires a unicorn buyer, it is not a good exit.

E. The rental support test

What it means: Ask whether the resale price can be justified by realistic rent after handover, net of service charges, vacancy, and fees.

Why it matters: As speculative momentum fades, more buyers anchor to yield. Gross yields sit at 7.2% for apartments and 5.0% for villas and townhouses, but with rent growth decelerating, the yield story has to be real rather than rhetorical. Use building-level data from the DLD Service Charge Index, not blunt market averages.

Questions to ask: What does this unit rent for on day one? What is the gross yield at my exit price? What survives after service charges, vacancy, and broker fees?

Red flags: Yield only works on aggressive rent assumptions, unusually high service charges, an area already seeing tenants gain negotiating power.

Green flags: Proven rental depth, realistic yield, manageable service charges, an income case that works without heroic rent growth.

Treat the rent line as the market’s lie detector.

F. The handover pressure test

What it means: Map how much stock moves from construction risk into cash-call reality around your project’s completion date.

Why it matters: Many investors do not fail because the project is bad. They fail because too many similar projects hand over at the same moment, forcing a wave of investors into the same exit window. And slippage does not save you.

Questions to ask: How much same-area stock is due in the six months around my handover? Are nearby projects actually on track? If delays occur, do they reduce my risk or push it into a bigger future cluster?

Red flags: Multiple nearby towers due together, many buyers likely needing to flip before final payment, a community entering its first major handover wave.

Green flags: Staggered delivery, proven absorption, few direct comparables in the same window.

Build a delivery calendar, not just a unit-level memo.

G. The developer inventory test

What it means: Check whether the developer still controls meaningful inventory in or near your project, and whether they are likely to discount quietly.

Why it matters: Developers have tools individual resellers do not: payment plans, broker incentives, bundled furniture, fee waivers, and the simple credibility of buying new. The rise in initial developer sales across both off-plan and ready segments is the clue here.

Questions to ask: How much stock does the developer still hold? Are they more likely to protect pricing or move inventory? Is there evidence of quiet incentives rather than headline cuts?

Red flags: Significant standing inventory, frequent promotional pushes, sales teams still actively placing units at similar pricing.

Green flags: Developer nearly sold out, strong handover record, little stock overhang.

Never assume you are selling into a free market if the developer still dominates supply.

H. The transferability and payment-plan test

What it means: Understand the contractual mechanics of selling before completion.

Why it matters: Resale is not just finding a buyer. It is whether the project lets you assign the unit easily enough for that buyer to say yes. The DLD requires a developer NOC to resell before title transfer, mortgaged property needs bank consent, and a completed unit only moves to title deed once fully paid.

Questions to ask: At what paid percentage can I assign? What are the NOC and transfer fees? Does a mortgage complicate the transfer?

Red flags: Assignment restrictions not disclosed up front, a large unpaid balance, legal friction around NOC or bank release.

Green flags: Clear written assignment terms, smooth Oqood transfer, no financing complications.

Ask for the exact assignment rules before you tell yourself the unit is liquid.

I. The scarcity test

What it means: Measure whether the unit has genuine scarcity value or just polished launch marketing.

Why it matters: Scarcity is what holds a premium alive when liquidity thins. Prime and genuinely scarce stock has held up far better than generic apartments through this softening.

Questions to ask: Could a buyer find something functionally identical within a ten-minute drive? Is this scarce by land, by format, by community maturity, or only by being “new”?

Red flags: A generic one-bed in a market full of generic one-beds.

Green flags: True waterfront, a rare villa typology, a proven family community, limited comparable future stock.

Scarcity is not a slogan. It is observable competition risk.

J. The buyer-after-you test

What it means: Define the next buyer in concrete terms. This is the master test that the other nine feed into.

Why it matters: If you cannot name the next buyer’s profile, equity, financing path, and reason to choose your unit, you do not have an exit thesis. Tellingly, Betterhomes reports buyer demand in Q1 2026 shifted toward larger homes, with apartment enquiries falling while villa and townhouse enquiries rose. The demand is moving. Your unit needs to be where it lands.

Red flags: Exit depends on “another investor like me.” No end-user case, no income case, no finance case.

Green flags: Clear end-user depth, visible landlord demand, a sensible price point, a financeable unit, a credible community story.

Write the buyer memo before you write the offer.

Who still wins

None of this is an argument against off-plan. It is an argument against the lazy version of off-plan. Strong deals still exist, and they tend to share a profile:

A scarce location with limited comparable future supply

Genuine end-user depth, not just investor churn

A strong developer with a clean delivery and transfer record

Proven rental demand that supports the price on yield alone

A rational entry price close to ready comps

A differentiated unit, view, or layout that is easy to explain

Infrastructure already in place or clearly committed

A buyer pool beyond speculators

In practice, that increasingly points toward townhouses and villas in maturing family communities, where supply is constrained relative to apartments and demand is shifting toward larger homes, and toward scarce prime and waterfront stock where comparison inventory is thin. In a slower market, it is easier to sell “a place to live” than “a phase in a masterplan.”

Who is most exposed

The mirror image. The highest-risk profile stacks several of these together:

Investor-heavy towers with little end-user demand

Apartment-heavy communities with clustered handovers, the corridors where the supply concentration is highest

Projects where the developer still holds competing inventory

Units bought purely to flip, with no hold case

A thin resale buyer pool

High service charges that crush net yield

Optimistic rent assumptions that the slowing rental market won’t support

Weak differentiation in a sea of identical units

Final-payment pressure near handover forcing a rushed exit

If a deal ticks four or five of these, the brochure is selling you the entry while hiding the exit.

Where AI actually earns its place

Let me show you the workflow I now run before I touch any off-plan unit, because this is the part most people get wrong about AI in real estate.

AI is not useful because it can write a property description or a glossy listing caption. That is marketing-layer noise, and the market is drowning in it. AI becomes useful at the underwriting layer: when it pressure-tests a sales brochure, compares your unit against real alternatives, surfaces the assumptions you’ve quietly made, and forces you to name the buyer after you before you commit capital.

The problem is that doing this well in normal Claude is repetitive. You’d have to re-explain the entire framework every single time: the ten checks, the weighting, the scoring bands, the rule that launch demand and resale liquidity are different things, the instruction to separate evidence from assumptions from missing data. Miss a step and the output drifts back into brochure mode, telling you what you want to hear.

So I stopped re-explaining it. I packaged the entire 2026 Off-Plan Exit Framework into a Claude Skill.

What a Skill actually is

A Claude Skill is a reusable instruction set you add to your own Claude account once. Think of it as hiring an analyst, training them on a specific methodology, and then having them apply that exact methodology on demand, forever, without re-briefing. Instead of pasting the framework into every chat, the Skill loads automatically whenever you ask Claude to assess an off-plan unit. Same rigour, same scoring, same discipline, every time.

The one I built is called the Dubai Off-Plan Resale Risk Analyst. Here’s how it runs:

You add it to Claude with a single click (no coding, no setup).

You drag in your data: a Property Monitor export, a REIDIN download, a Buildable comp set, an SPA, a payment schedule, whatever you have.

You name the unit and ask it to assess the exit.

It returns a structured exit-resilience score out of 100, with red flags, green flags, a defined buyer-after-you, and best-case, base-case, and stress-case exit paths.

Critically, it does not tell you “buy” or “don’t buy.” It does something far more useful: it separates what you actually know from what you’re assuming from what you’re missing, and it refuses to fake the gaps. If you don’t give it the ready comps or the supply pipeline, it caps its own confidence and tells you exactly what to go and verify. That is the difference between an analyst and a brochure.

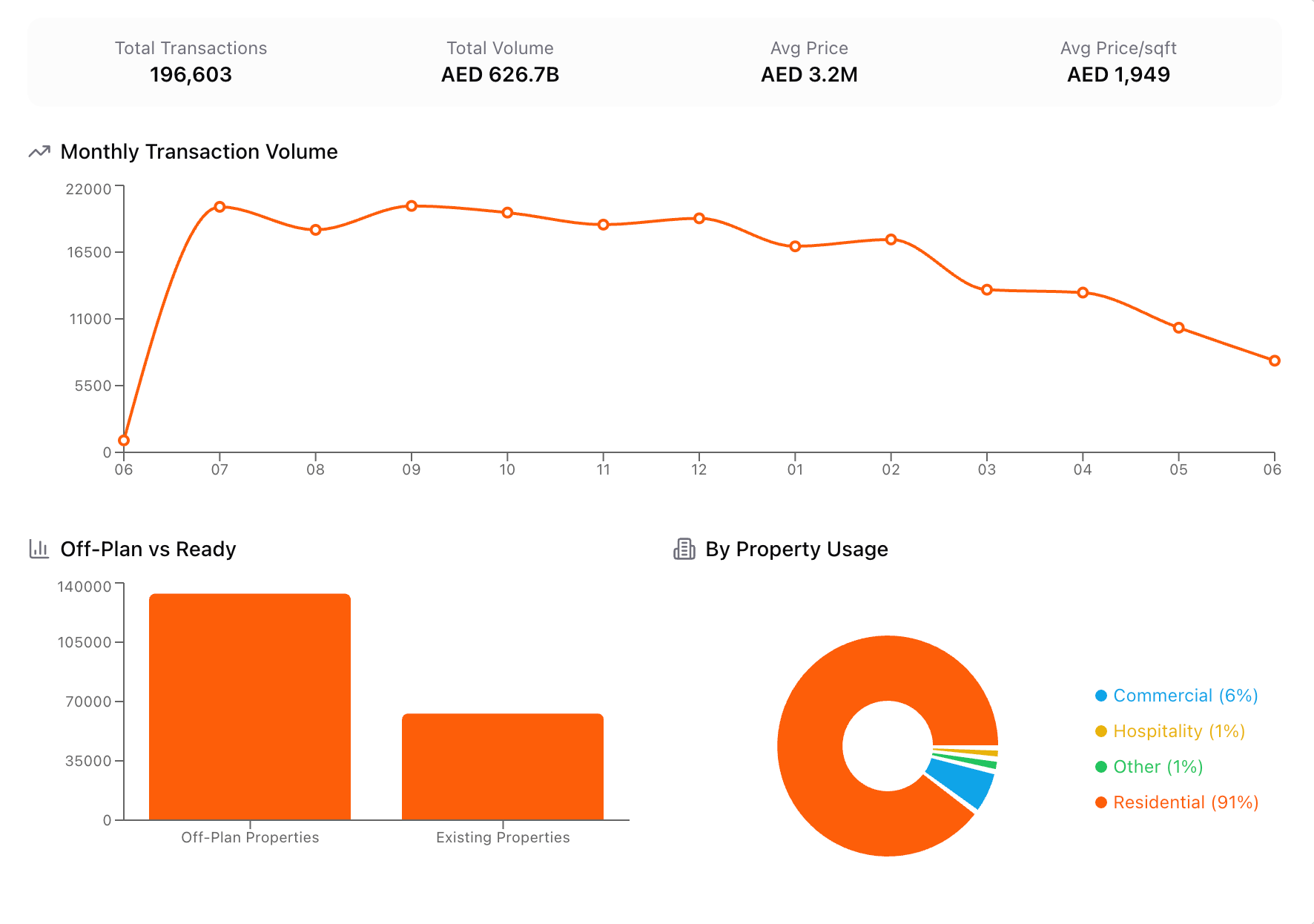

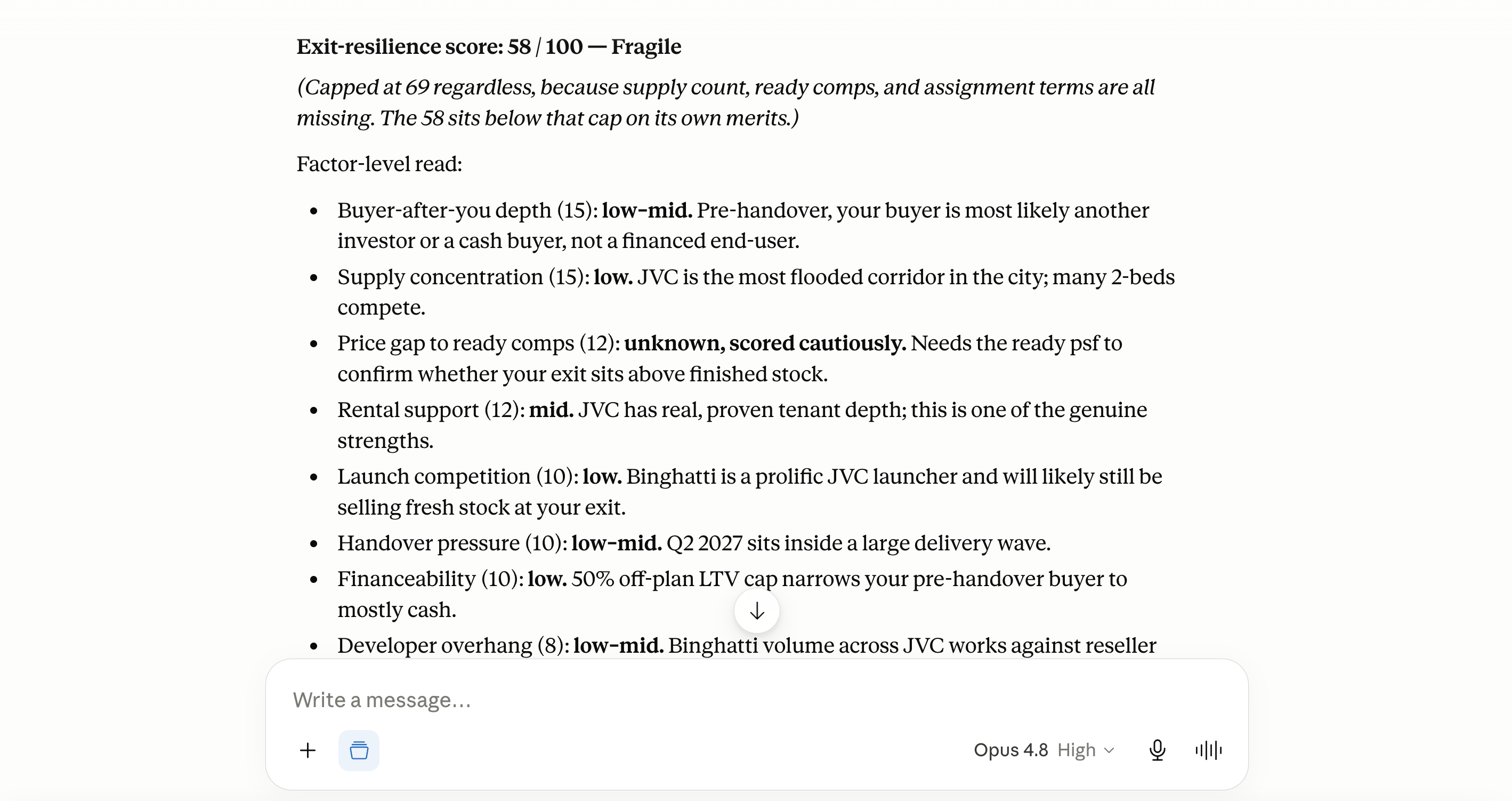

Here’s what that looks like in practice on a real JVC project:

Look at what’s happening in that output versus what vanilla Claude gives you. Ask normal Claude “is this a good off-plan deal?” and you get a confident, agreeable, generic answer in thirty seconds. Ask the Skill, and it interrogates the deal against ten weighted factors, flags that a pre-handover JVC exit collides with the 50% mortgage cap and the most saturated supply corridor in Dubai, and tells you the one genuine strength worth holding onto. One is a chatbot. The other is a risk desk.

And this is the real point I want to leave you with, beyond this single tool: this is how the underwriting layer of real estate gets rebuilt. The legwork the Skill depends on, pulling the supply counts, the transacted comps, the off-market context behind each number, is exactly what we built Buildable to automate. Buildable gathers the data; the Skill scores the exit. Together they turn a process that used to take a broker, a spreadsheet, and a week of phone calls into something you run before lunch.

I’ve packaged the Skill, and a lot more, into Real Brief Pro.

Here’s what being a Pro member actually gets you, beyond this week’s tool:

The Dubai Off-Plan Resale Risk Analyst Skill. The one-click tool from this article. Add it to your Claude, drag in your data, and underwrite any unit’s exit in minutes instead of an afternoon. Full install guide included (2-minute setup).

A 30-day trial of Buildable. The engine underneath the Skill. Our growing arsenal of real-estate-specific AI agents that map forward supply, pull and clean transacted comps, track developer inventory, and surface the off-market context that no portal records. The Skill scores the exit; Buildable does the legwork that feeds it.

Access to our investor database. REX, our searchable database of real estate investors by geography, ticket size, asset class, and strategy: family offices, institutional LPs, debt funds, GPs, and HNWIs. Pro members get a discount code (just message me).

A free AI implementation consultation. If you’re thinking about how to deploy AI at the company level, not just as a chatbot but as actual underwriting infrastructure, I’ll walk through it with you one-on-one.

If you are buying, selling, brokering, or advising on Dubai off-plan in 2026, this is the framework I’d want in front of me before touching the next launch, plus the tools to run it.

🔒 Real Brief Pro

👉 Upgrade to unlock the Skill download and your Pro benefits

Everything above is the framework. What’s below is the tool that runs it. Pro members get:

The Dubai Off-Plan Resale Risk Analyst Skill (add to your Claude in one click)

The install guide (2-minute setup)

If you are buying, selling, brokering, or advising on Dubai off-plan in 2026, this is the framework I’d want in front of me before touching the next launch. Use this link to download the skill file: